Over the last decade, sustainability reporting has evolved from largely voluntary and fragmented disclosures toward increasingly standardized frameworks designed to support financial decision-making. As discussed in HPL’s previous blog posts on the evolution of sustainability reporting and the adoption of IFRS S1 and S2 in Latin America, markets are progressively moving toward a more consistent disclosure landscape.

This transition is evolving in certain countries.. According to the IFRS Foundation, as of September 2024, 30 jurisdictions around the globe had already decided to use or were taking steps to introduce ISSB Standards into their legal or regulatory frameworks, representing approximately 57% of global GDP and more than 40% of global market capitalization.[1] In Latin America, regulatory developments related to IFRS S1 and S2 have emerged in jurisdictions such as Chile and Mexico, while Brazil has recently revisited its approach to mandatory sustainability disclosure requirements, highlighting that implementation pathways across the region continue to evolve. [2][3]

Greater disclosure does not automatically translate into better investment decisions. Investors today face an increasing volume of sustainability-related information, but challenges around comparability, usability, and consistency continue to limit how effectively that information can be incorporated into investment analysis. As sustainability disclosure frameworks continue to evolve, the conversation is shifting from what companies should disclose to whether sustainability information is actually influencing investment decisions and capital allocation.

Comparability: The Missing Link in Sustainable Investing

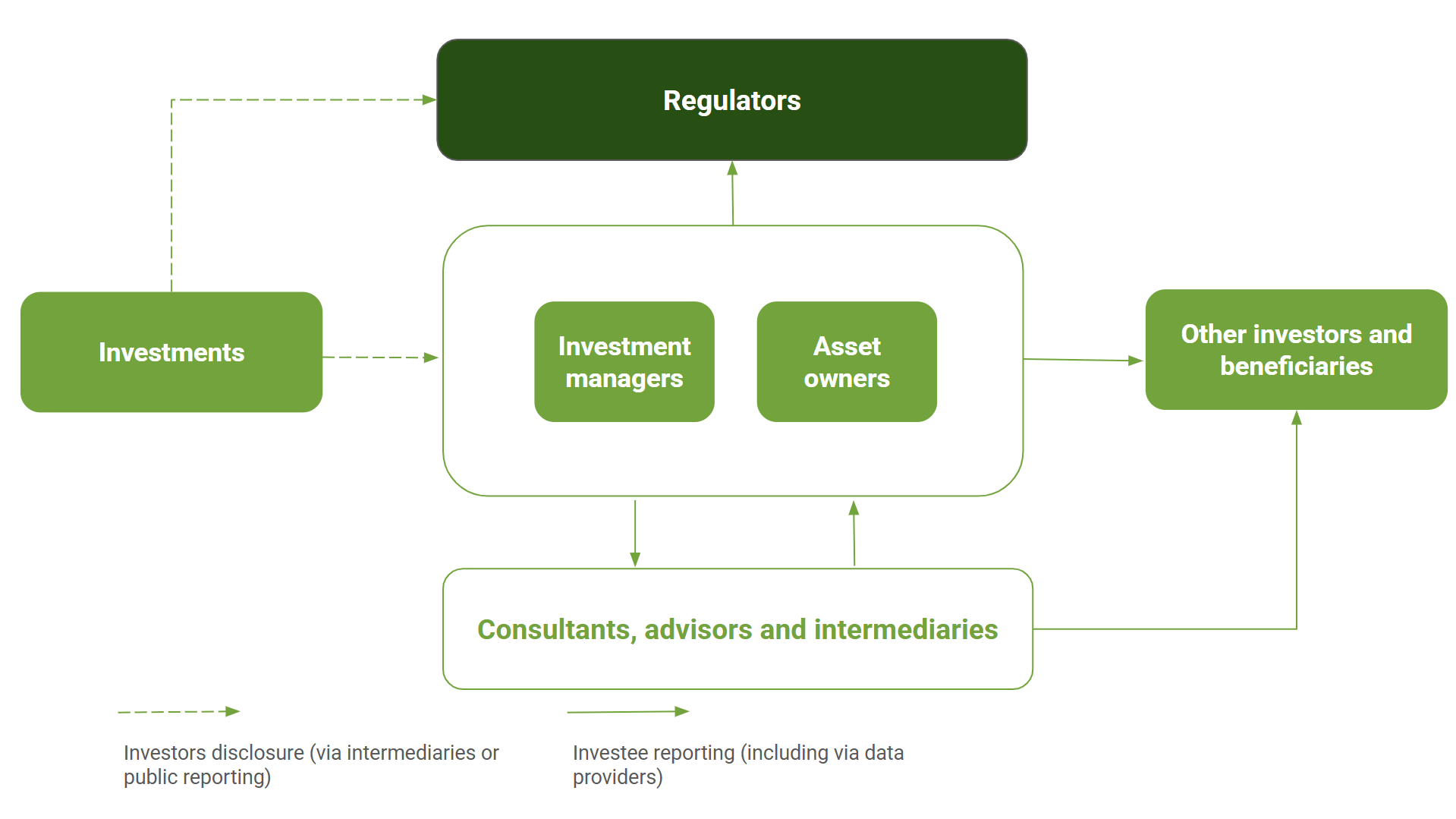

The growing complexity of sustainability disclosure ecosystems is increasing the importance of comparability across markets and market participants. Sustainability-related information now flows through multiple actors, including issuers, investors, intermediaries, regulators, and data providers (see Figure 1), each with distinct reporting needs and expectations. [4]

Figure 1. The ecosystem of sustainability disclosure and investment decision-making

Source PRI 2026

Today, investors review a broad range of sustainability-related information, including corporate sustainability and climate disclosures, allocation and impact reports for thematic bonds, and sustainability-linked bond (SLB) targets, and, to a lesser extent, ESG ratings. However, the growing availability of sustainability data does not necessarily make investment decisions easier. In practice, sustainability information only becomes useful when investors can interpret it consistently across issuers, sectors, jurisdictions, and financial instruments.

Certain disclosures are increasingly becoming baseline expectations for investors seeking to integrate sustainability considerations into investment processes. In corporate reporting, investors often prioritize comparable indicators such as greenhouse gas emissions, climate targets, governance practices, and transition-related metrics. In sustainable debt markets, investors also rely on transaction-specific disclosures, including use of proceeds reporting, KPI definitions, and alignment with frameworks such as the ICMA Principles to assess the credibility and transparency of thematic bond issuances.[5][6]

Institutional investors interviewed by HPL consistently emphasized the importance of comparability as a foundation for informed investment decision-making, enabling effective benchmarking, risk evaluation, and portfolio construction across sustainability-oriented strategies. At the same time, investors acknowledged that differences in methodologies, reporting boundaries, and sector realities continue to complicate comparisons across companies and markets, particularly in emerging economies where disclosure practices remain uneven.[7]

Recent PRI research also highlights an important tension between standardization and flexibility. While investors increasingly depend on standardized baseline disclosures to compare risks and performance across issuers, many also recognize that sustainability information cannot always follow a one-size-fits-all approach. Sector realities, transition pathways, and product-specific considerations often require additional context and flexibility beyond standardized indicators alone.[4]

What Investors Actually Value in Sustainability Data

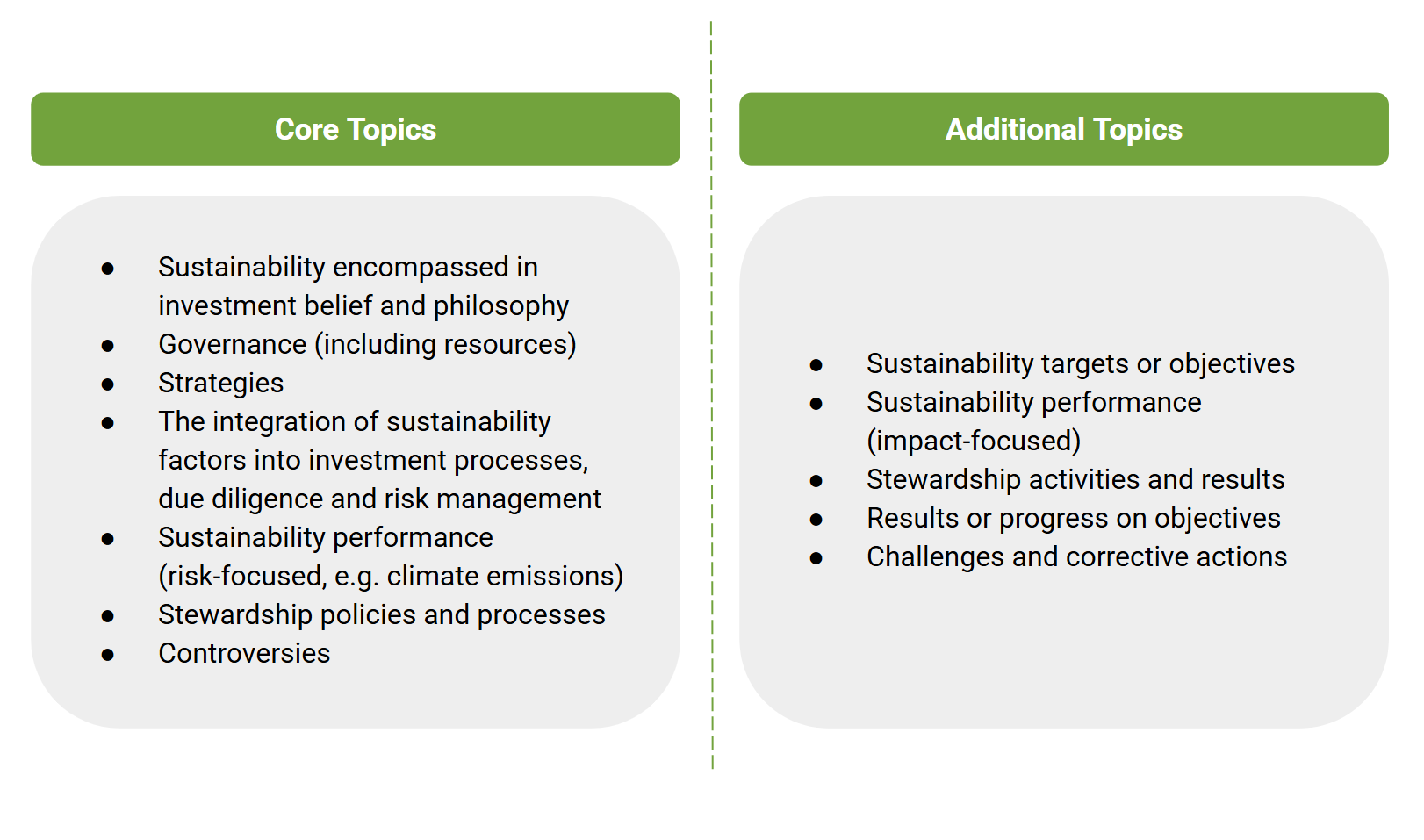

However, investors are increasingly differentiating between information that is broadly expected and information that genuinely strengthens investment analysis and decision-making. While some disclosures primarily serve transparency or compliance purposes, others are more directly connected to how investors assess risks, credibility, transition readiness, and long-term value creation (see Figure 2).[4]

Figure 2. Core and additional disclosure topics

Source: PRI 2026

Recent discussions around ISSB implementation and investor disclosure practices suggest that sustainability information becomes significantly more valuable when it can be connected to financial performance, transition resilience, and long-term value creation. Increasingly, investors are looking for sustainability information that helps them understand potential impacts on cash flows, business strategy, operational resilience, and access to capital, rather than disclosure that remains purely compliance-oriented.[8] This is also reflected in MSCI’s 2025 sustainability outlook, which highlights that investors increasingly use sustainability-related data to assess competitiveness, profitability, long-term resilience, and cost of capital dynamics across companies and sectors.[9]

Conversations conducted by HPL with institutional investors reinforce this trend. Interviewees consistently emphasized the importance of quantitative metrics, transparent methodologies, external verification, and transaction-specific reporting that can be integrated into internal investment processes and assessment frameworks.[7] In sustainable debt markets specifically, investors highlighted disclosures related to use of proceeds allocation, KPI calibration, impact reporting, and sustainability-linked targets as particularly valuable when assessing the credibility and ambition of thematic bond issuances. [7]

Several interviewees also noted that strong sustainability disclosure can directly influence internal assessments, investment conviction, and participation from sustainability-focused investors, particularly when reporting demonstrates credible transition strategies and clear alignment between sustainability commitments and broader business objectives.[7]

What Makes Sustainability Data Hard to Use

Despite the progress toward more structured sustainability disclosure, investors still face practical challenges when interpreting and using non-financial data across institutions, sectors, and projects. PRI research points to a growing misalignment between investors’ data needs, what disclosure frameworks require, and the capacity of reporting entities to prepare useful information, particularly when data is not relevant, accessible, or credible enough to support decision-making.[4]

Interviews conducted by HPL reinforced this gap. Investors noted that sustainability information is often dispersed across corporate reports, websites, data providers, impact reports, and PDF-based disclosures, making it difficult to aggregate or integrate into internal systems. In sustainable debt markets, this challenge is especially visible when comparing allocation and impact reporting across issuers, where differences in methodologies, reporting boundaries, timing, and assumptions can limit comparability and increase the burden of analysis.[7]

Data interpretation also remains a key challenge. Investors highlighted that even when issuers report on similar indicators, such as greenhouse gas emissions, avoided emissions, or SLB targets, differences in calculation methods and levels of assurance can affect confidence in the data. [7]

Finally, transparency can also be constrained by market and political dynamics. Some interviewees noted the rise of “greenhushing,” where companies continue sustainability-related work but reduce public communication due to regulatory, or political concerns. This creates a difficult balance: investors need more consistent and usable information, but issuers may face legal, competitive, or reputational constraints when deciding how to disclose.[7]

Together, these challenges show that the next phase of sustainability reporting is not only about increasing disclosure volume. It is about improving the relevance, quality, comparability, accessibility, and credibility of the information investors actually need to make decisions.

Conclusion: From Transparency to Capital Allocation

The rapid evolution of sustainability disclosure frameworks reflects a broader shift in financial markets: sustainability information is increasingly expected to support investment decisions, not simply reporting exercises. As investors incorporate sustainability considerations into risk assessment, portfolio construction, and stewardship activities, the relevance of comparability, credibility, and decision-useful information will continue to grow.

At the same time, this transition also highlights an important reality: more disclosure does not automatically lead to better investment outcomes. Investors increasingly value sustainability information that is financially relevant, methodologically robust, and capable of supporting real-world investment analysis across sectors, markets, and financial instruments. As sustainability reporting frameworks continue to mature, the next challenge for issuers, regulators, and market participants will not only be improving transparency, but ensuring that sustainability disclosure can effectively support more informed capital allocation decisions and long-term transition financing.

—

Brenda Aguilar is an Associate at HPL. She graduated with honors from the Law School of the Universidad Nacional Autónoma de México (UNAM), where she also completed the Advanced Postgraduate Course in Financial Law. In addition, she graduated with special honors from the Bachelor’s Degree in Financial Management at the Instituto Tecnológico Autónomo de México (ITAM). At HPL, she has supported the execution of 18 consulting projects related to the structuring of GSS+ bond frameworks for financial institutions, development banks, and corporates across Latin America and the Caribbean (LAC), Eastern Europe, and Africa. She has also contributed to sustainable finance initiatives through research, comparative studies, capacity building, and sustainable finance strategy analysis.

—

[1] IFRS Foundation (2024). Progress on Corporate Climate-related Disclosures—2024 Report. Available here.

[2] HPL (2026). IFRS S1 and S2 in Latin America: A New Era of Sustainability Disclosure. Available here.

[3] Capital Reset (2026). CVM cede à pressão e derruba obrigatoriedade de reportes de sustentabilidade. Available here.

[4] Principles of Responsible Investment (PRI) (2026). Towards decision-useful investor sustainability disclosure). Available here.

[5] ICMA (2024). Impact Reporting Handbook and Guidance. Available here.

[6] IFRS Foundation (s.f.). Introduction to the ISSB and IFRS Sustainability Disclosure Standards. Available here

[7] HPL investor interviews conducted for this article.

[8] CFA Institute, IFRS Foundation, and PwC (2025). Sustainability Reporting: Global Trends and Implications for Investment Analysis. Available here.[9] MSCI (2025). Sustainability and Climate Trends to Watch 2025. Available here.