As global climate goals grow more urgent, emerging markets face a dual challenge: how to grow their economies while reducing emissions from carbon-intensive sectors that still power their development. Unlike green finance, which focuses on environmentally sustainable projects such as renewable energy or clean transportation, transition finance is aimed at supporting sectors and activities that are emissions-intensive today but have credible, time-bound pathways to align with a low-carbon, climate-resilient economy.[1]

This distinction is particularly relevant for emerging markets, where rapid development and rising energy needs drive continued reliance on carbon-intensive sectors, contributing significantly to global emissions.[2] Transition finance provides a pathway to align climate goals with development priorities, allowing for gradual and credible decarbonization in contexts where immediate green alternatives may not be technologically or economically feasible.

Understanding the distinction between green and transition finance is crucial, but equally important is identifying where the greatest need and opportunity for transition lies.

The Opportunity for Emerging Markets

Emerging markets are becoming a driving force in global energy dynamics, as rapid economic expansion, industrialization, and urban growth continue to push energy demand upward. As highlighted in TCW’s Sustainable Insights (2024), these economies increasingly require more energy to sustain their growing cities and industries, fueling higher consumption and sustained investment in infrastructure.[3] Citing data from the IEA, the report notes that emerging markets are expected to outpace developed economies in energy demand growth over the coming decade, driven by structural factors such as urbanization, industrial expansion, and rising living standards. Adding to the challenge, emerging and developing economies already account for nearly two-thirds of global greenhouse gas emissions, making their transition pathways critical to meeting global climate targets.[4]

While renewable energy will play a leading role in this shift, full decarbonization is unlikely to occur in a single step, especially in regions where access, cost, or technical readiness still pose challenges. Transition finance can bridge this gap by supporting investments that fall outside traditional green taxonomies but contribute meaningfully to emissions reductions. Within the energy sector, this includes fuel-switching technologies, low-carbon hydrogen, ammonia infrastructure, grid modernization, and transitional upgrades to more energy efficient fossil-based systems, particularly in hard-to-abate sectors such as heavy industry and transport.[5]

Several corporate issuers in Latin America have begun to explore transition finance as a pathway to support sectoral decarbonization. In Brazil, a range of transition-labeled instruments have been issued across energy, infrastructure, and agribusiness. For example, Marfrig, a leading meat producer, issued a USD 500 million transition bond in 2019 linked to responsible cattle sourcing in the Amazon region. Eneva, an integrated energy company, has issued multiple transition debentures since 2020 to support investments in lower-emission thermal generation, such as natural gas. More recently, Vibra Energia and CCR RioSP have structured domestic transition bonds to finance activities including energy efficiency, cleaner fuels, and biodiversity protection. These examples reflect growing experimentation in applying transition finance to high-emission sectors in emerging markets, even as market standards and taxonomies continue to evolve.[6]

Beyond macro-level trends, individual countries have begun implementing transition finance tools at scale. Japan’s Climate Transition Bonds provide a concrete example of how public-sector leadership can help define standards and scale investment in hard-to-abate sectors. In early 2024, the government issued the world’s first sovereign transition bonds, backed by its national Green Transformation (GX) Strategy, with the goal of mobilizing JPY 20 trillion over the next decade. Proceeds are being allocated across 22 fields, including hydrogen and ammonia production, next-generation solar, carbon recycling, and decarbonization initiatives in sectors such as steel, transport, agriculture, and energy infrastructure.[7]

What sets Japan’s program apart is the combination of clear project eligibility criteria, sectoral roadmaps, and mandatory emissions reduction plans from beneficiary companies. The framework has earned certification from the Climate Bonds Initiative and the Japan Credit Rating Agency for its alignment with the Paris Agreement.[8] It has also been praised for its transparency, cross-sector integration, and catalytic role in crowding in private investment to support long-term transition goals.

To enable the scaling of initiatives like Japan’s and ensure consistency across issuers, several frameworks have emerged to guide the market. These tools help define what constitutes a credible transition, offering clarity and confidence to both issuers and investors.

Frameworks and Tools to Support Transition Finance

As the market for transition finance evolves, the development of credible frameworks is essential to guide financial institutions, issuers, and investors in structuring transactions that are aligned with long-term climate goals. Two widely recognized tools: the Climate Transition Finance Handbook, the Climate Transition Bond Guidelines and the Transition Loan Principles, provide practical guidance for ensuring the integrity and effectiveness of transition-labelled instruments.

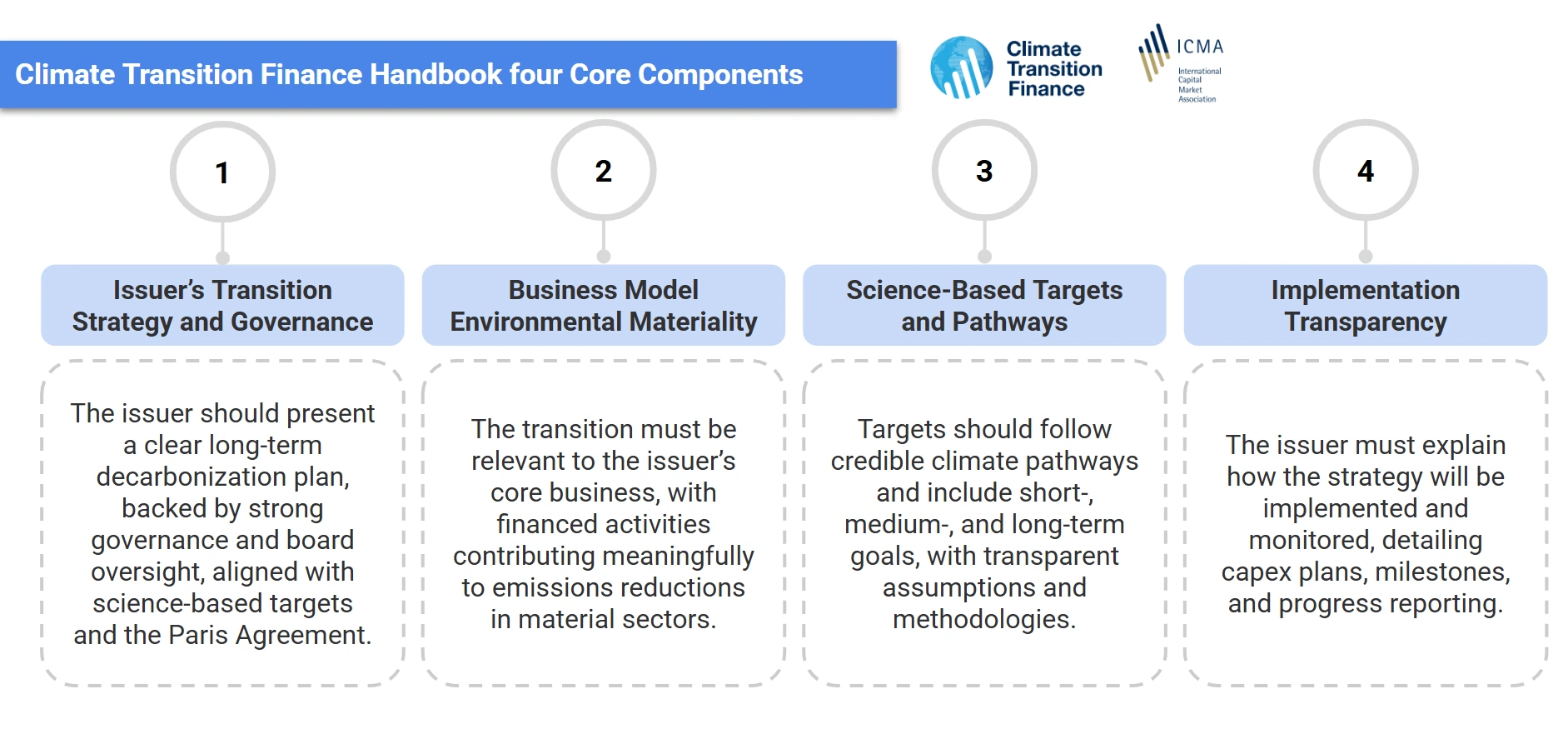

Climate Transition Finance Handbook (CTFH)[9]

The CTFH establishes voluntary guidance for the design of financial instruments aimed at supporting the transition to a low-carbon economy. Its approach is based on four fundamental pillars that provide benchmarks for assessing the credibility of bond issuances labeled as transition bonds, in line with the objectives of the Paris Agreement. These pillars offer a useful framework for ensuring integrity, traceability, and transparency in channeling capital to issuers with robust decarbonization plans.

Figure 1. Core Components of the Climate Transition Finance Handbook

These four pillars seek to ensure that emissions labeled as “transitional” are not merely nominal, but reflect verifiable and ambitious commitments to real transformation. By demanding consistency between strategy, use of funds, and measurable impact, the CTFH strengthens the credibility of these types of instruments in the face of risks such as greenwashing or lack of alignment with global standards.

While the guidelines discussed later in this document provide more detailed and specific criteria across the thematic finance pillars, the CTHF primarily serves as a conceptual and disclosure framework. It frames transition finance as a tool for issuers to reduce GHG emissions within their core business over time and/or diversify into low-carbon activities, anchored in a science-based strategy (ideally aligned with 1.5°C and, at minimum, well below 2°C). It also encourages robust, decision-useful disclosure, covering the transition plan (e.g., detailed CapEx plans), just transition considerations, and broader environmental and social externalities. In addition, it recommends granular reporting on CapEx/OpEx plans, internal carbon pricing assumptions, phase-out strategies, alignment metrics, and both qualitative and quantitative assessments of carbon lock-in emissions and mitigation measures.

One opportunity to strengthen transparency around the transition strategy outlined in the CTFH is to conduct transition assessments. These act as a “traffic light,” signaling how credible the strategy is and how it could be financed. They also support due diligence for banks, investors, and insurers, and help prioritize efficiency and decarbonization projects with clear business cases.

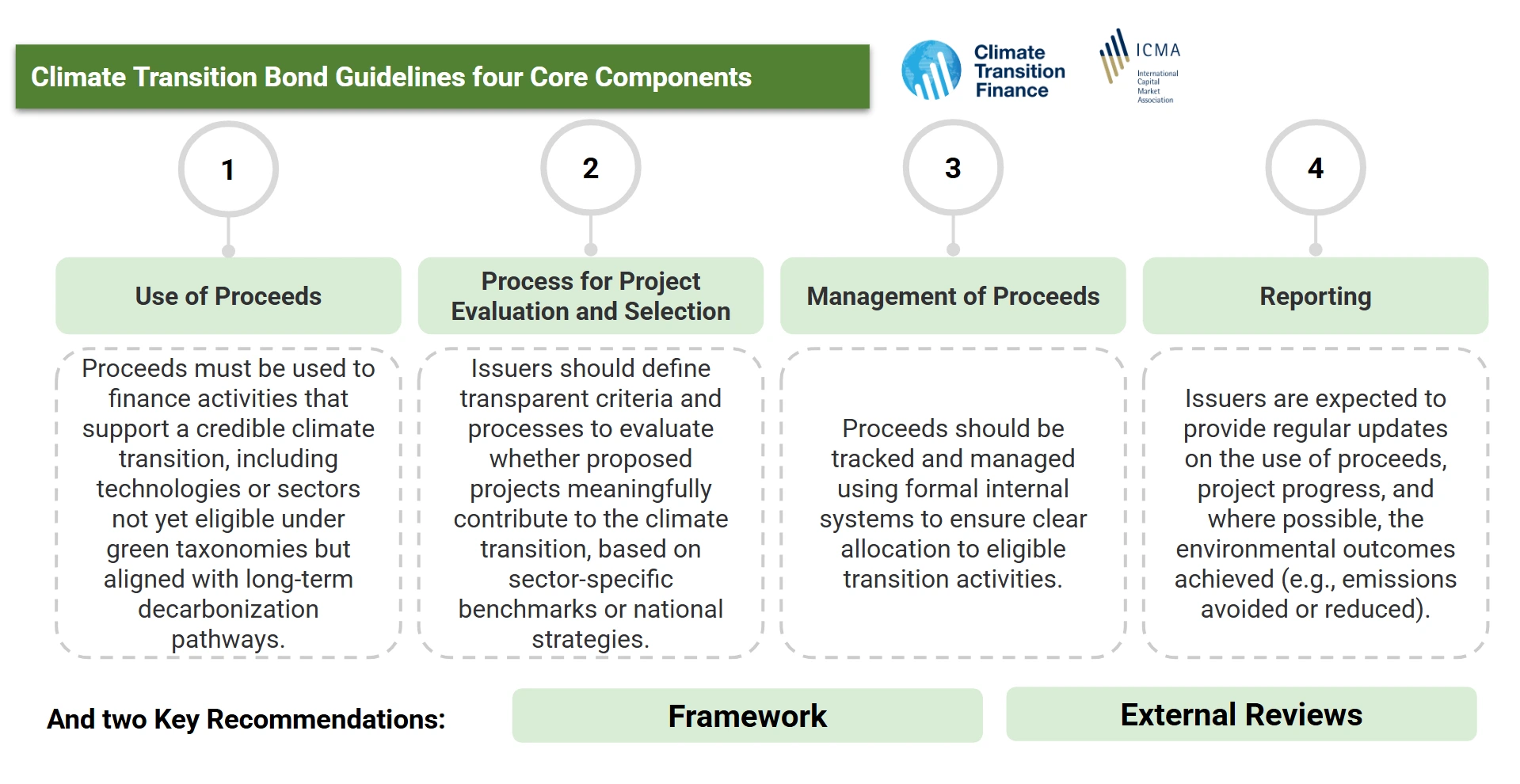

Climate Transition Bond Guidelines (CTBG) [10]

The CTBG provides a market-oriented framework to support the issuance of credible transition bonds by both sovereign and corporate actors. Designed to reflect the evolving nature of decarbonization, especially in high-emitting and hard-to-abate sectors, the CTBG aims to ensure that proceeds are aligned with climate transition strategies, while remaining flexible enough to apply across diverse national contexts. The guidelines emphasize alignment with the Paris Agreement, sectoral pathways, and transparent reporting mechanisms as central conditions for transition eligibility.

Figure 2. Core Components of the CTBG

The guidelines defines Climate Transition (CT) Projects to include assets, investments, and activities, as well as R&D and early phase-out/decommissioning, within emissions-intensive sectors, with the objective of achieving quantifiable GHG avoidance, reduction, or removal that goes beyond business-as-usual (BAU), leveraging best available technologies where feasible. The guidelines require issuers to have an issuer-level transition strategy explicitly linked to the financed projects and aligned or compatible with relevant taxonomies, decarbonisation pathways, and climate policy frameworks. The principles also require issuers to identify, mitigate, and disclose carbon lock-in risks, and to substantiate, through evidence such as cost-benefit analysis, the technical and economic infeasibility of lower-carbon alternatives in the issuer’s context. Additional safeguards apply where projects relate materially to fossil-fuel infrastructure or activities, including asset-level transition plans, phase-out commitments, clear milestones and sunset dates, and constraints on capacity expansion or lifetime extensions, among others. The principles provide a non-exhaustive list of eligible categories and mandate that eligibility criteria be reviewed and updated periodically to reflect evolving standards and technological progress. Finally, the principles recommend an independent external review, covering both a pre-issuance assessment and post-issuance verification of the tracking and allocation of proceeds.

These components work together to ensure that transition-labeled bonds are grounded in strategic intent, credible project selection, and measurable outcomes. The CTBG seeks to balance flexibility with rigor, enabling innovation while maintaining market integrity, so that transition bonds can serve as trusted instruments in financing climate-aligned development.

Transition Loan Principles (TLP)[11]

The Transition Loan Principles provide a specific framework for loans with funds used to finance activities that do not yet qualify as “green” but are on track to align with climate goals. Through five essential components, the TLP seeks to establish criteria that ensure the integrity and climate impact of these instruments, thereby facilitating financing for sectors that are difficult to decarbonize.

Figure 3. Key Components of the TLP

The principles specify that UoP should be allocated to eligible CapEx, OpEx, R&D, and phase-out/decommissioning expenditures that are on a credible net-zero pathway, delivering clear, measurable, and substantial GHG reductions within a defined timeframe. They also require the loan to be anchored in an entity-level transition strategy supported by project selection grounded in recognized sector pathways and scenarios (e.g., IEA/IPCC), as well as taxonomies and public policy frameworks. In addition, the project evaluation and selection process incorporates environmental and social risk assessment, just transition considerations, carbon lock-in risk analysis, and an assessment of the technical and economic feasibility of lower-carbon alternatives in the local context. Finally, the principles recommend independent external review pre-issuance and the verification of use-of-proceeds allocation and reported impacts.

By structuring these five components, TLPs enable financial institutions to mobilize resources toward projects with transformative potential, even when they still face technological or regulatory constraints. This framework helps bridge the gap between the operational reality of emitting sectors and global climate goals, promoting an orderly and verifiable transition.

Taken together, the CTFH, CTBG, and TLP frameworks offer complementary guidance for structuring credible transition finance instruments. The CTFH serves as a high-level disclosure and strategy framework, outlining principles for issuer-level alignment and transparency. In contrast, the CTBG focuses specifically on the design of labeled transition bonds, introducing project-level criteria, lock-in safeguards, and a taxonomy-linked approach to ensure environmental integrity. The TLP, tailored for the loan market, provides the most detailed criteria across entity- and project-level alignment, requiring robust justifications, science-based strategies, and sectoral benchmarks. While each framework varies in scope and application, they all converge on the need for measurable GHG reduction, credible transition pathways, and strong governance to build trust and scale capital flows toward net-zero goals.

These frameworks collectively provide the foundation for a more coherent and trustworthy transition finance ecosystem, one that bridges ambition with accountability.

Key Challenges

1. Evolving Policy and Regulatory Context

In many markets, transition finance operates in the context of evolving policies, disclosure requirements, and taxonomies. The absence of stable, long-term policy signals and consistent regulatory frameworks can make it more difficult for issuers, financial institutions and/or investors to assess risks and structure financing for transition-aligned activities. This may contribute to uncertainty in decision-making and project development.[12] The Climate Transition Bond Guidelines (CTBG) attempt to address this by setting clear expectations for issuer-level alignment, project eligibility, and safeguards, yet market-wide convergence remains a work in progress.

2. Data and Measurement Limitations

Reliable, forward-looking data is essential to assess the credibility of transition activities, particularly regarding emissions trajectories, sectoral pathways, and corporate transition plans. However, data availability remains uneven, especially in emerging markets and private-sector issuers. While transition planning is becoming more widespread, the depth, comparability, and alignment of such plans with climate goals still vary considerably, making it difficult to benchmark and track real progress.[13]

3. Technology Readiness and Risk of Stranded Assets

In many high-emitting sectors, low-carbon technologies are either not yet commercially viable or lack the scale to be cost-effective in emerging market contexts. This technological gap can delay the implementation of transition strategies, even when capital is available. At the same time, the rapid pace of innovation and evolving regulatory frameworks increase the risk of stranded assets, investments that may lose economic value prematurely due to shifts in policy, market conditions, or technological obsolescence. This uncertainty complicates long-term financing decisions and underscores the importance of flexible, forward-looking transition plans. Frameworks like the CTBG and TLP explicitly call for the identification and mitigation of lock-in risks and recommend that issuers justify the technological and economic feasibility of financed activities, promoting more informed, forward-looking investment decisions.

Conclusion

Transition finance is not simply a financial tool, it is a structural enabler for emerging markets navigating the dual challenge of economic development and climate responsibility. Rather than assuming that high-emitting sectors can be excluded from the climate finance conversation, transition finance acknowledges their centrality and seeks to support their evolution through credible, science-aligned pathways.

What distinguishes transition finance is its ability to operate in the real economy, where the path to decarbonization is incremental, sector-specific, and capital-intensive. By focusing on transition rather than exclusion, it creates space for pragmatic solutions, particularly in regions where energy demand is growing and infrastructure transformation is essential. Sovereign leadership, robust taxonomies, and integrated policy frameworks can help convert these principles into investable opportunities.

Transition finance is more than a niche product, it is a strategic lever to unlock inclusive, climate-aligned development. In the decade ahead, how capital is directed in emerging markets will define not just national economies, but the world’s ability to meet its climate goals.

—

María Fernanda Benítez, recently graduated with a Bachelor’s Degree in Actuarial Science from the Instituto Tecnológico Autónomo de México (ITAM). At HPL, she has contributed to the execution of 5 consulting projects by conducting research, performing comparative studies, structuring thematic Bond Frameworks and preparing reports for development banks and sovereigns in LAC. Previously, Fernanda worked at Citigroup as a ICG Operations Summer Analyst, where she conducted comparative analysis of KPIs and collaborated in implementing improvements in tracking processes. Prior to this, she was an intern at Samsung Electronics Mexico, where she generated detailed reports on training-related KPIs and contributed to the creation of innovative materials. Her focus is on finance, sustainable finance, consulting, and corporate banking.

—

References

[1] CFA Institute. (2024). Navigating Transition Finance: An Action List. Available here.

[2] Sustainalytics. (2025). Opportunities to Finance Reduced Emissions in Emerging Markets. Available here.

[3] TCW. (2024). Navigating the Future of Energy: The Growing Power Demand in Emerging Markets. Available here.

[4] Ibid.

[5] NatWest Group. (2025). Climate and Transition Finance Framework and Target. Available here.

[6] HPL. (2025). Internal Bond Market Database. Not available online.

[7] Government of Japan (2024). Climate Transition Bonds Show Japan’s Commitment to Carbon Neutrality. Available here.

[8] Ibid.

[9] ICMA. (2025). Climate Transition Finance Handbook. Available here. (2024). Five Key Barriers to Transition Finance. Available here.

[10] ICMA. (2025). Climate Transition Bond Guidelines. Available here.

[11] LMA. (2025). Guide to Transition Loans. Available here.

[12] RMI (2024). Five Key Barriers to Transition Finance. Available here.

[13] CFA Institute. (2024). Navigating Transition Finance: An Action List. Available here.