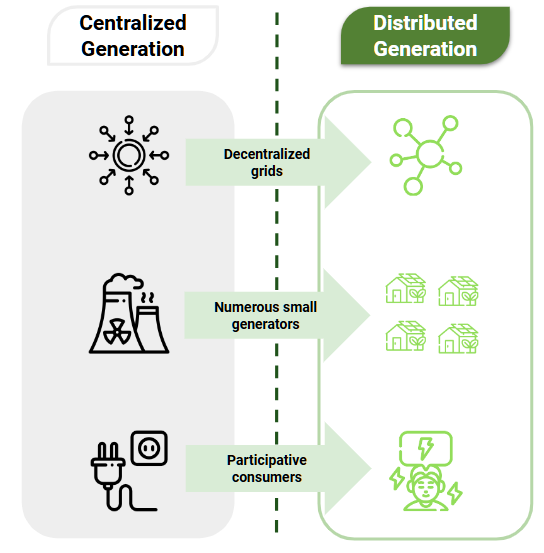

Energetic systems, in the context of a just and inclusive energy transition, are facing substantial changes in their way of generating, selling, distributing, and consuming these resources. Electrification, which is a key condition for the clean energy transition, is increasing power consumption and the quantity and variety of electrical equipment that can shift their demand. In this context, Distributed Generation (DG) systems play an important role. DG encompasses various technologies that produce electricity close to or at the location where it will be consumed. They are decentralized and bidirectional distribution systems that help consumers be more proactive in the power markets [1]. Figure 1 illustrates the difference between centralized and DG systems.

Figure 1. Comparing Centralized and Distributed Generation Systems

Distributed energy resources (DER) -which includes storage of energy, heat pumps and electric vehicles (EVs)- give users a central role by decentralizing grids and by lowering generation scale [2]. Promoting DER is one strategy that can be applied to face the challenges of the energy transition aligned with the 1.5°C climate goal. DER can help increase the resilience of the system through the reduction of distances between generators and consumers, distribution bottlenecks, and dependence on large generators. DG and EVs can have a symbiotic relation, as EVs increase the electric demand and increase economic incentives for DG and offset these additional costs. Additionally, if run on renewable energy systems, they can help to displace fossil fuel-based generation and reduce related emissions. From an economic perspective, in some cases DER can lower bill costs for “prosumers” (energy consumers that also become producers)[3]. Finally, from a social point of view, DER can be applied to widen energy access in areas without connection to the grid [4] [5].

Renewable DG has witnessed a huge expansion in the last decades globally. Distributed Photovoltaic Systems (PVs), EVs, and heat pumps account for most of the recent DER expansion. Some trends help explain this growth:

- The IEA has estimated that 167 GW of distributed PV were added globally from 2018 – 2021, with 64% of new capacity coming from China, Europe and the United States.

- Global EV stock has tripled between 2017 – 2020, and

- Global Stock for heat pumps increased nearly 10% per year from 2015 – 2020 [6].

When analyzing the Latin American and Caribbean (LAC) landscape, there are some interesting insights regarding DG implementation. In LAC, 50% of solar PV capacity is deployed on distributed generators. Brazil and Mexico are the largest markets for this source, with more than 90% of the installations across the region. Since 2007, installed capacity of Distributed PV, an average of 120% annually, reaching 31.7 GW and more than 2.9 million users [7].

LAC demonstrates a competitive advantage for the development and deployment of new clean generation technologies, such as renewable DG, not only due to its abundant renewable resources (61% of the grid is sourced by renewables [8]), but also because of its high percentage of urban population (80%). DER in cities can help lower distribution bottlenecks and stabilize the grid by reducing distances between generation and consuming nodes and by creating smaller and more resilient microgrids. This justifies the relevance of decentralized electric generation technologies.

Further expansion of DER will face challenges related to obsolete legal frameworks and high costs of capital. To unleash its full potential, governments and financial institutions should promote broader access to the technology by updating legal frameworks and promoting public policies and financial incentives for further deployment.

Updating Legal Frameworks for DER Deployment

Legal Frameworks that regulate renewable DG in LAC have not been updated to reflect current realities. They were developed in the early 2000s, when energy systems relied on large, centralized generators, and distributed resources were a less mature technology. Policy makers were afraid of being incapable of controlling a decentralized grid and established strict limits to the expansion of DER [9].

For example, in the Dominican Republic, there is a law (the Reglamento de Interconexión Generación Distribuida) that sets penetration caps of DG below the technical capacity. DG cannot exceed 15% of the annual peak demand of the network [10]. Today, this cap limits the expansion of installed capacity, mainly in urban areas where new solar panels are not allowed to be installed. This limits the potential of the deployment of Distributed PV systems. A study commissioned by the GIZ estimates that urban Dominican grids have the potential to manage between 75% to 150% of distributed capacity. To achieve greater deployment of these technologies, legal frameworks will need to be updated in order to allow for their application [12].

Public Policies Providing Financial Incentives to DER

Compared to centralized systems, DERs are more expensive because their costs per unit of energy (Levelized Cost of Energy, LCOE) tend to be higher than utility or commercial scale projects [13]. Public policies and financial incentives are needed to support further deployment.

There are a few examples of public policies that have been applied to incentivize renewable DG. One alternative is through promoting community distributed generation. Community solar generation is a specific type of renewable DG implementation where a group of users installs a single generation system and shares the associated benefits. Community schemes allow lower investments, shared operation and maintenance (O&M) costs, and can also increase the scale of the solar park [14]. The government of Córdoba in Argentina is working towards a payment scheme through blockchain that aims to unlock investments from people who are not connected to the provincial grid. Through this government incentive, Córdoba will pay through tokens the green energy generated and also for the emissions saved [15].

Brazil, which has more than 70% of the total installed renewable DG capacity of LAC, has several government programs that help in broadening access to DER . One example is included within the affordable housing program Minha Casa Minha Vida (MCMV). MCMV is a housing initiative of the Brazilian federal government, created by President Lula in March 2009, which offers subsidies and reduced interest rates to make the purchase of affordable housing more accessible, both in urban and rural areas, with the aim of combating the country’s housing deficit. In 2023, the federal government included solar panels as eligible to be financed within the program. Additionally, prosumers will receive a discount of 50% of the energy they consume from the grid. This program, focused on low-income families, is expected to develop more than 2,000,000 houses until 2026 [16]. The installation of solar panels will reduce by 85% the cost of electricity of the program’s house energy bills [17].

Opportunities

Having discussed the main insights of DER in Latin America and the Caribbean, we can argue that updating legal frameworks and ensuring broader access to technology are key challenges.

Current laws often lag behind the evolving energy landscape, hindering the expansion of distributed generation, especially in urban areas with untapped technical capacity. Additionally, financing remains a major barrier to widespread adoption. Many countries in LAC have tax exemptions for the installation of solar PV panels in distributed facilities. Nevertheless, they are mainly related to the commercial and industrial sectors, sectors that also pay a lower energy value. Residential users are not included in tax incentives programs which reduces their access to generation capacity.

More inclusive policies and accessible programs are needed to expand access to DG, particularly for vulnerable and low-income communities. There are successful initiatives, such as including solar panels in housing programs or blockchain apps for investing in panels, which can lower the individual investment of each prosumer by offering fractions of an communitary installation. Public policies are a cornerstone to drive widespread adoption of renewable energy.

In summary, while renewable DG offers numerous benefits, including emissions reduction, less dependence on subsidies, and increased energy resilience, its full potential will only be realized with updated legal frameworks and adequate financing. Governments, financial institutions, and other key stakeholders must collaborate to overcome these challenges and leverage the opportunities of distributed generation for sustainable energy transitions in the region.

—

Luis Wagner is an analyst at HPL, graduated with a Bachelor’s degree in International Relations from the University of San Andrés (UdeSA). He is currently pursuing a Master’s degree in Sustainable Energy Development at the Buenos Aires Institute of Technology (ITBA). He has experience working in energy transition, public policies, international cooperation and communication strategies.

—

References

[1] PNUMA. (2022). Estado de la Generación Distribuida Solar Fotovoltaica en América Latina y el Caribe. Available here.

[2] IEA. (2022). Unlocking the Potential of Distributed Energy Resources. Available here.

[3] ENEL (2023). Prosumers: when energy consumers become energy producers. Available here.

[4] IEA. (2022). Unlocking the Potential of Distributed Energy Resources. Available here.

[5] Kazimierski, M. (2021). Generación distribuida de energía renovable ¿una oportunidad para la desconcentración del sistema energético argentino? Available here.

[6] IEA. (2022). Unlocking the Potential of Distributed Energy Resources. Available here.

[7] PNUMA. (2022). Estado de la Generación Distribuida Solar Fotovoltaica en América Latina y el Caribe. Available here.

[8] IEA. (2024,). Renewables 2023 Analysis and forecasts to 2028. Available here.

[9] PNUMA. (2022). Estado de la Generación Distribuida Solar Fotovoltaica en América Latina y el Caribe. Available here.

[10] Comisión Nacional de Energía. (2012). Reglamento de Interconexión Generación Distribuida. Santo Domingo, Dominican Republic. Available here.

[12] GIZ. (2021). Estudio de Nivel de Penetración Fotovoltaica Permisible en las Redes de Distribución Dominicana. Available here.

[13] Yale Environment (2023). Understanding the Value of Distributed Energy Resources. Available here.

[14] PNUMA. (2022). Estado de la Generación Distribuida Solar Fotovoltaica en América Latina y el Caribe. Available here.

[15] Chamorro, A. N. (2022). Convertirse en un “token”, el próximo paso de las energías renovables en Córdoba. Available here.

[16] FotoVolt. (2023,). Novo Minha Casa, Minha Vida inclui geração solar distribuída. Available here.

[17] EPBR. (2023). Entenda a nova lei que prevê painéis solares no Minha Casa Minha Vida. Available here.